-

Since the 24th February 2022, Russia has been conducting extensive air and missile strikes against the Ukraine military they have also been conducting concurrent ground offensives beyond Crimea and the Donbas breakaway entities. Recent reports highlighted that Russia has continually advanced in different maneuver axes and at present, no one can predict when and how the Ukraine conflict will end. For over three months, the conflict has greatly influenced the global economy and sounded the alarm bells for global food safety, especially to those countries which greatly depend on food and chemical fertilizer import from Russia and Ukraine, as well as those countries sensitive to food price variation shock.

According to the '2021 GLOBAL REPORT ON FOOD CRISES (GRFC 2022)' by the World Food Program (WFP) and Food and Agriculture Organization of the United Nations (FAO), due to regional conflicts, economic downturn and Covid-19 about 1.93 billion people in 53 countries and regions are facing a food crisis, which is the highest number since 2016, and since 2000 the number has increased by 0.4 billion. Since both Russia and the Ukraine are important countries for grain export, the Russia-Ukraine conflict, the reduced agricultural output (particularly grains and oilseeds), and economic sanctions against Russia, have further enhanced the global food crisis. Notably, we are facing great challenges in global food safety. Here, we try to emphasize the influences of the Russia-Ukraine conflict on global food safety in terms of its short- and long-term effects based on our current understooding to date.

Agriculture in Ukraine and Russia -

Ukraine was derived from the former Soviet Union and gained independence in August 1991. Located at a latitude of 44°−52° N, Ukraine has a temperate continental climate for most of the region with a subtropical climate in the south. The maximum annual precipitation is 2,000 mm in the Karpatian region, 970 mm in the Polysiers region, and 500 mm in the southern region. The average temperature in January is −7.4 °C, with an average temperature in July of 19.6 °C. It is inhabited by over 41 million citizens and covers an area of 603,700 km2.

In the former Soviet Union, more than 20% flour, 55% vegetable oil, 44% pork and 83% of sugar were provided by Ukraine. Agricultural land is about 42.56 million hm2, accounting for about 70% of the land area. Twenty three percent of the world's black land is distributed in Ukraine. Ukraine's arable land was 33.403 million hm2, with a utilization rate of 99.5%; grassland area was 2.16 million hm2, with a utilization rate of 93.7%; pasture was 4.762 million hm2, with a utilization rate of 93.2%. The main agricultural products are wheat, barley, corn and sugar beets.

In 2020, GDP per capita in Ukraine amounted to US

$\$ $ $\$ $ https://ihsmarkit.com ).Russia is divided into seven federal districts; however, most of the agricultural production takes place in 'European' Russia, the regions that border Ukraine and Belarus, and stretch 3,000 miles to western Siberia in the east. The main grain production areas are the Central and Southern districts, neighboring Volga and then also Siberia, and to a lesser extent the Urals. Production in the country is dominated by cereals, most notably wheat, with oilseeds also maintaining a strong market position led by sunflower, soybeans and oilseed rape. Russia accounted for 3.8% of the world commercial seed market in 2020, making it the seventh-largest seed market and the largest within Europe. Despite strong growth over the last decade, in 2020, Russia's seed sales in USD terms, declined by 1.3% to US

$\$ $ $\$ $ $\$ $ $\$ $ Both Russia and Ukraine are big exporters of agricultural products. According to USDA data (

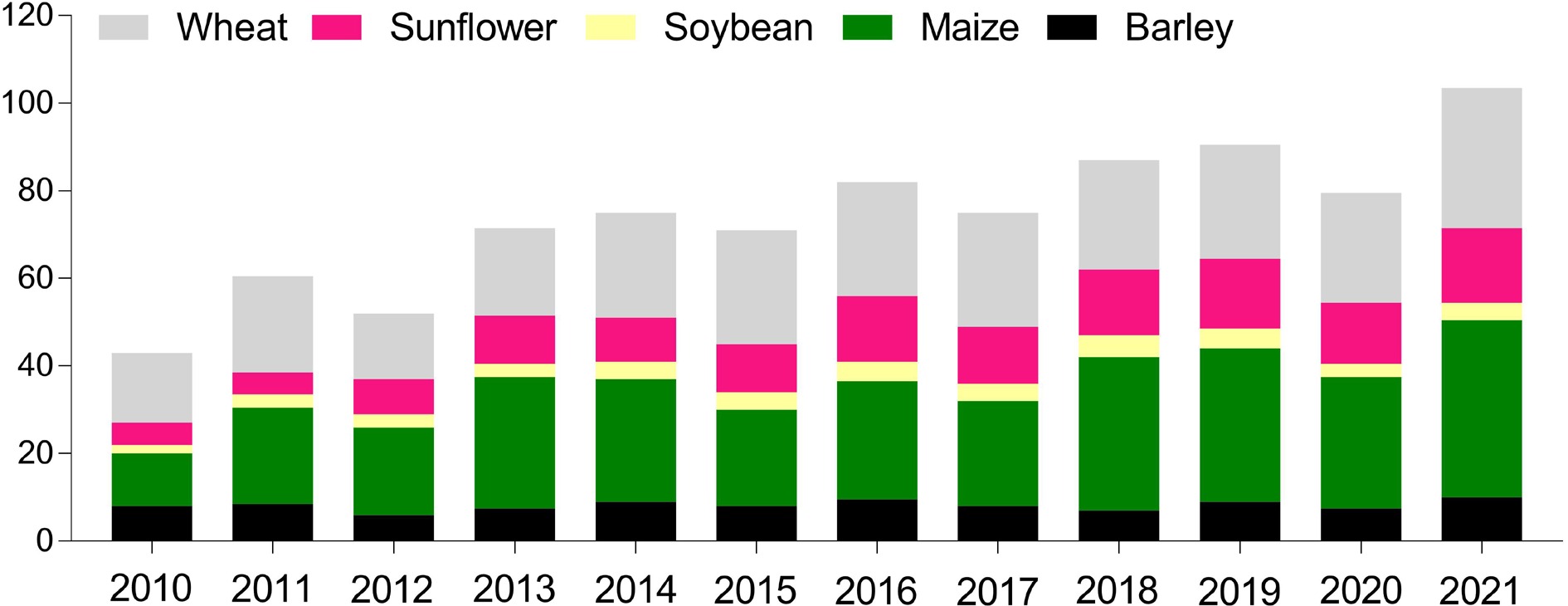

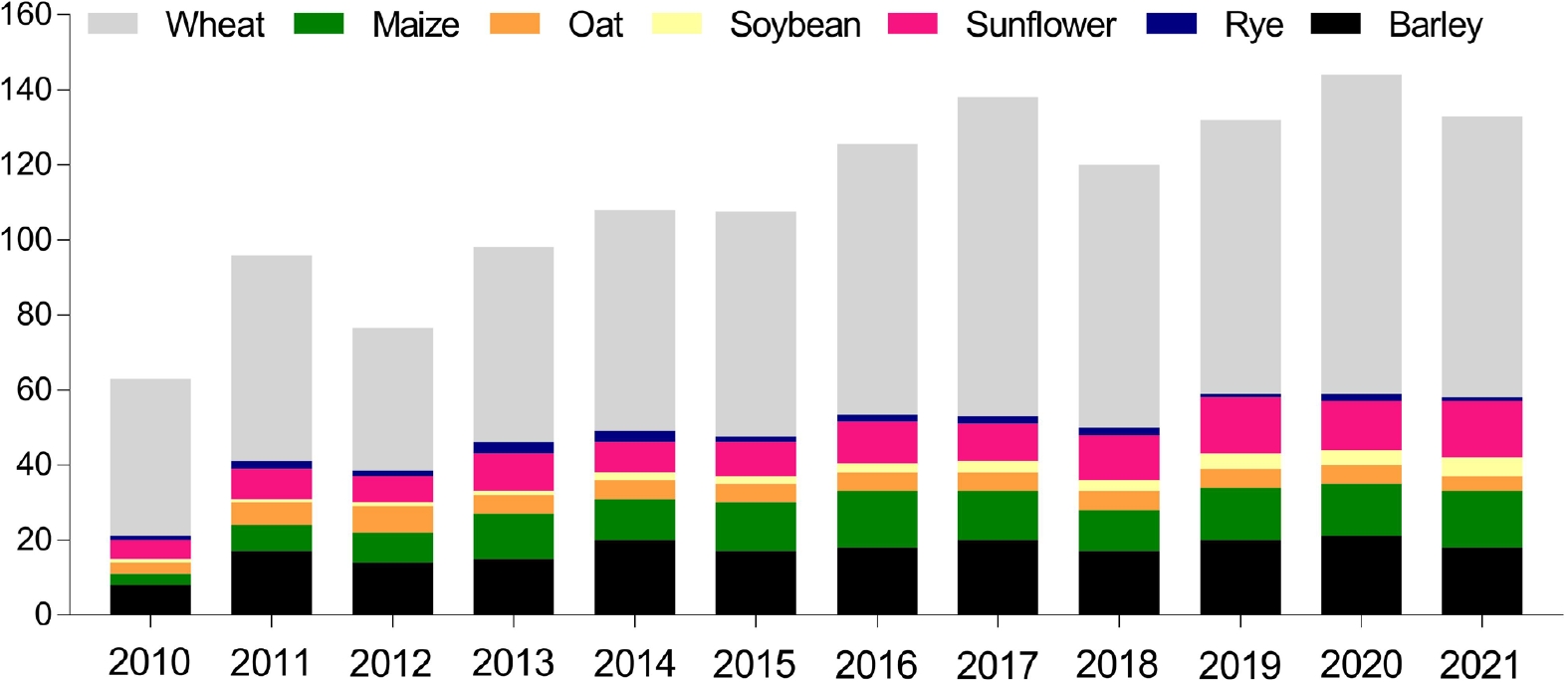

www.usda.gov/topics/data ), from the average of export share in 2017−2021, Russia and Ukraine accounted for 30% of global wheat exports, 20% of maize, 76% of sunflower oil, 32% of barley. In addition, corn production worldwide is about 1.21 billion tons, of which Russia and Ukraine contributed 15 million tons (1.2%) and 42 million tons (3.5%), respectively. Figures 1 and 2 show the major crop distribution and yield (Source: CITIC Futures Research Department,www.citicsf.com/e-futures ), indicating their positions in the global food market.

Figure 1.

Major crop production in Ukraine.

Figure 2.

Major crop production in Russia.

The impact of the conflict on agriculture in Ukraine and Russia -

The Russia-Ukraine conflict has already lasted over three months. The economy, especially agricultural activities are obviously disrupted. According to the latest report from CCTV (China) regarding the current conflict situation, about 1/4 of the region has been involved in the military fighting and economic activities have been interrupted. The Russian military still steadily push forward to the central part of Ukraine, and it is hard to predict when and how the conflict will end. If the situation worsens for both Russia and Ukraine, the global economy will suffer a heavy blow and food security will be unprecedently challenged.

From the Russian perspective, although agricultural activities are not yet notably influenced by the conflict, several aspects may impact its agricultural economy.

(1) Western sanctions have extensively influenced the overall economy, including agriculture.

(2) As a major grain exporter Russia has to give up some traditional markets and find new markets to back its normal agricultural production. This may impact the global food supply and demand balance.

(3) Russia and Belarus are key mining and production regions for potash, and Russia is a relevant source of nitrogen, a raw material for nitrogen fertilizer, and natural gas. The conflict and subsequent western sanctions have greatly disturbed the global market from Russian potash and nitrogen fertilizers.

(4) As the war continues more labour and factories will be reutilized for military use, and overall reduced labor resources for agriculture can be expected.

From the Ukrainian perspective, there are several challenges which may influence its current agriculture.

(1) Ukraine mainly depends on financial assistance from Western countries and it is difficult to retain as much government input as usual for agriculture currently and in near future. It is difficult for foreign investors to invest in Ukraine agriculture.

(2) Crop planting area has been greatly reduced. The eastern Ukraine region to which Donetsk and Luhansk makes up the bulk of the black soil area. Agricultural activities in this area are greatly interrupted or no longer controlled by Ukraine government due to its claimed independence.

(3) Ukrainian famers are holding their inputs in the land to avoid further economic losses until the conflict is resolved. However, it is not clear how and when the conflict will end, farmers can do nothing but wait. Spring crop sowing has been missed, and summer has arrived, but the situation remains unclear.

(4) Labor for agriculture are likely becoming soldiers or supporting workers for the conflict. Additionally, some of the laborours have fled to neighboring countries as refugees. Therefore, it is difficult to organize efficient agricultural activities as previous, even in the areas not yet involved in the conflict.

(5) Energy costs keep increasing and farmers have to input much more to maintain normal production.

(6) Most of the Ukrainian exports are being carried out through ports on the Black and Azov Seas — Odessa, Pivdeny, Chornomorsk, Kherson, Mariupol, and Berdyansk. According to IHS Markit data (

https://ihsmarkit.com ), in 2020, 56.4% of total Ukrainian exports were transported by sea. However, this route is now blocked and the majority of famers still hold their grain. According to the Associated Press, on July 22, an agreement between Russia and Ukraine on the Ukrainian grain export was signed in Istanbul, Türkiye. The pathway has been opened for millions of tons of urgently needed Ukrainian grain, but whether the impasse that threatens peripheral food security can be truly ended will still depend on the smooth implementation of the agreement.(7) Fertilizer production and transportation are influenced, which may not only increase the difficulties of Ukrainian agriculture but also impact the global fertilizer market.

As the conflict continues, its future impact on agriculture and global food security is unclear. It depends how long the conflict will last. No matter when it ends the effects are already being seen in Ukraine, Russia, Europe and the global grain market.

The short-term effects of the conflict on global food safety -

As the Russian-Ukraine conflict has lasted for over three months, the impact has already been seen in the global oil and grain market. However, the influence of the conflict on agricultural activities in the short-time, on other countries is not yet notable. The major and direct effects are seen in Ukraine, countries which depend on grain and fertilizer import from Russia and Ukraine are also likely be affected.

The direct impact of the conflict is the transportation block. The head of Ukraine's Maritime Administration confirmed on the 28th February 2021 that Ukrainian ports will remain closed until the Russian invasion ends, adding that the port of Mariupol has sustained damage from Russian shelling. Moreover, multiple shipping companies have suspended sailings to the endangered Black Sea ports. Additionally, at least three commercial ships have been hit by bombs since the 24th of February 2021. Ukrainian President Zelensky has said that about 20 million to 25 million tons of grain in Ukraine cannot be transported, and by the fall of this year, this figure may reach 70 million to 75 million tons. Ukraine's large amounts of grains cannot be quickly exported although a agreement has been made for food transportation as mentioned above, which has pushed up global food prices and put pressure on countries that rely on wheat imports, particularly in the Middle East and Africa.

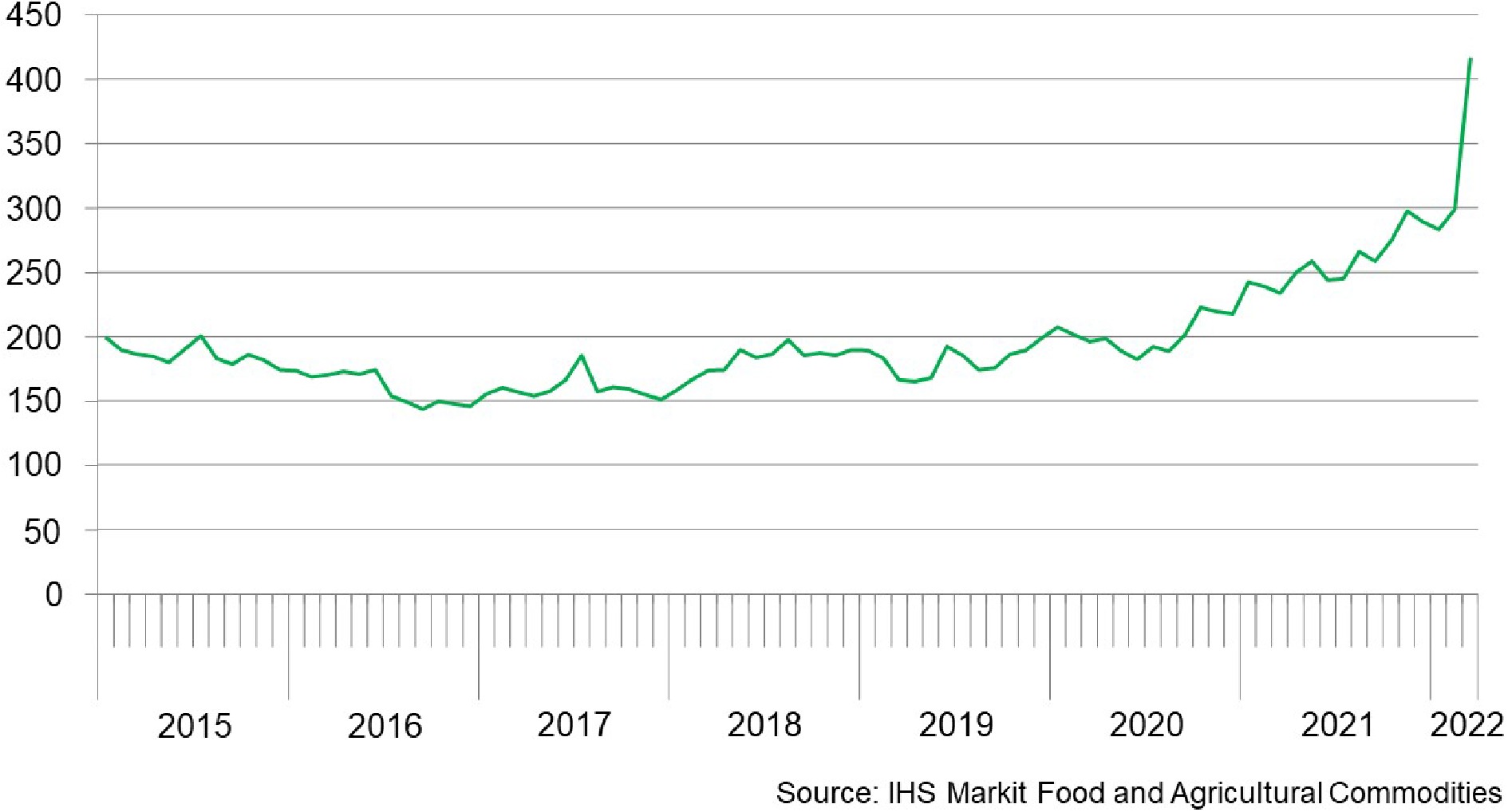

Another direct effect of the conflict is that grain production will continue to be reduced in 2022. On 18th May 2022, Ukraine's Minister of Agricultural Policy and Food Solskyi said in an international conference that Ukraine's grain production is likely to drop by 50% this year, and the sowing of winter crops will also be seriously affected. The international community should be prepared to raise the price of wheat per ton from US

$\$ $ $\$ $

Figure 3.

Wheat-CBOT Chicago SRW Wheat Futures (USD/Ton).

Table 1. Major export destinations for Ukrainian and Russian wheat 2021.

Rank Ukraine Russia Destination Value of trade ($\$m) Destination Value of trade ($\$m) 1 Egypt 858 Türkiye 1,802 2 Indonesia 727 Egypt 1,548 3 Türkiye 446 Azerbaijan 292 4 Pakistan 354 Nigeria 254 5 Morocco 232 Kazakhstan 215 6 Bangladesh 217 Sudan 203 7 Yemen 206 Bangladesh 188 8 Saudi Arabia 186 Latvia 176 9 Tunisia 163 Saudi Arabia 172 10 Ethiopia 161 Yemen 153 HS Code 1001

Source: IHS Markit Global Trade Atlas (https://ihsmarkit.com/products/maritime-global-trade-atlas.html )China is also one of the countries that imports grain from both Russia and Ukraine. In 2020/21, China imported a total of 1.7 million tons of sunflower oil, of which 64% was imported from Ukraine. Ukraine is China's second largest importer of corn, customs data showed that from January to November 2021, China's cumulative imports of corn was 27.02 million tons, the United States and Ukraine are China's two major importers of corn, of the 19.59 million tons of corn imported from the United States, 7.315 million tons were imported from Ukraine, accounting for 27% of corn imports. Russia's state agricultural regulator said on Friday, 4th February 2022: 'China and Russia have adopted a bilateral agreement to lift regional restrictions on Russian exports of wheat and barley to China and allow wheat and barley to be exported to China throughout Russia'. This means that agricultural trade between the two countries will be further strengthened, so that even if the conflict between Russia and Ukraine continues to escalate, the impact of China on grain imports in the future will be minimized. However, for sunflower oil, China may need new providers.

As major fertilizer producers and exporters, Ukraine and Russia provide their Nitrogen (N), Phosphorus (P), and Kalium (K) to different countries worldwide, mainly to India, Brazil and Latin America. India depends heavily on imports of all three N, P, and K, however, they secured potash and N from new suppliers and thus India’s immediate needs have been met. Potash is the critical fertilizer in Brazil for soybean production. Brail imports 40% of its potash from Russia and Belarus. Brazilians are preparing their soybean season, which starts in September. They will enter the market in the following months to secure fertilizers. Latin America needs N for wheat and corn, global N supplier complex is fairly fragmented, and it is easier to find alternative solutions. China is not significantly influenced except by the increased energy price.

The long-term effects of the conflict on global food safety -

It is still too early to accurately estimate how the conflict may influence global food security as it depends on when and how the conflict ends. However, some of the effects over the following years can be estimated.

The Ministry of Agricultural Policy and Food of Ukraine lowered the sown area of the main crops this year from 16.92 million hectares to 13.44 million hectares. At present, Ukraine has missed the spring sowing season and most of the large grain growers are still in a 'wait-and-see' state, fearing that if the armed conflict does not end by the summer, they will miss next season and the normal cycle of the agriculture will be totally disrupted, which will need some time to reorganize following the war. In addition, 70% of Ukrainian agricultural light diesel is purchased from Belarus and Russia. Since the beginning of March, there has been a nationwide oil shortage in Ukraine, and the use of oil is strictly regulated. In western Ukraine, fuel supply is relatively abundant, but major oil depots and gas stations still impose restrictions on agricultural oil. Even after the war, this situation will remain or at least be difficult to recover since oil shortage is a general problem in EU. Ukraine agriculture may be affected by the results of the conflict for many years.

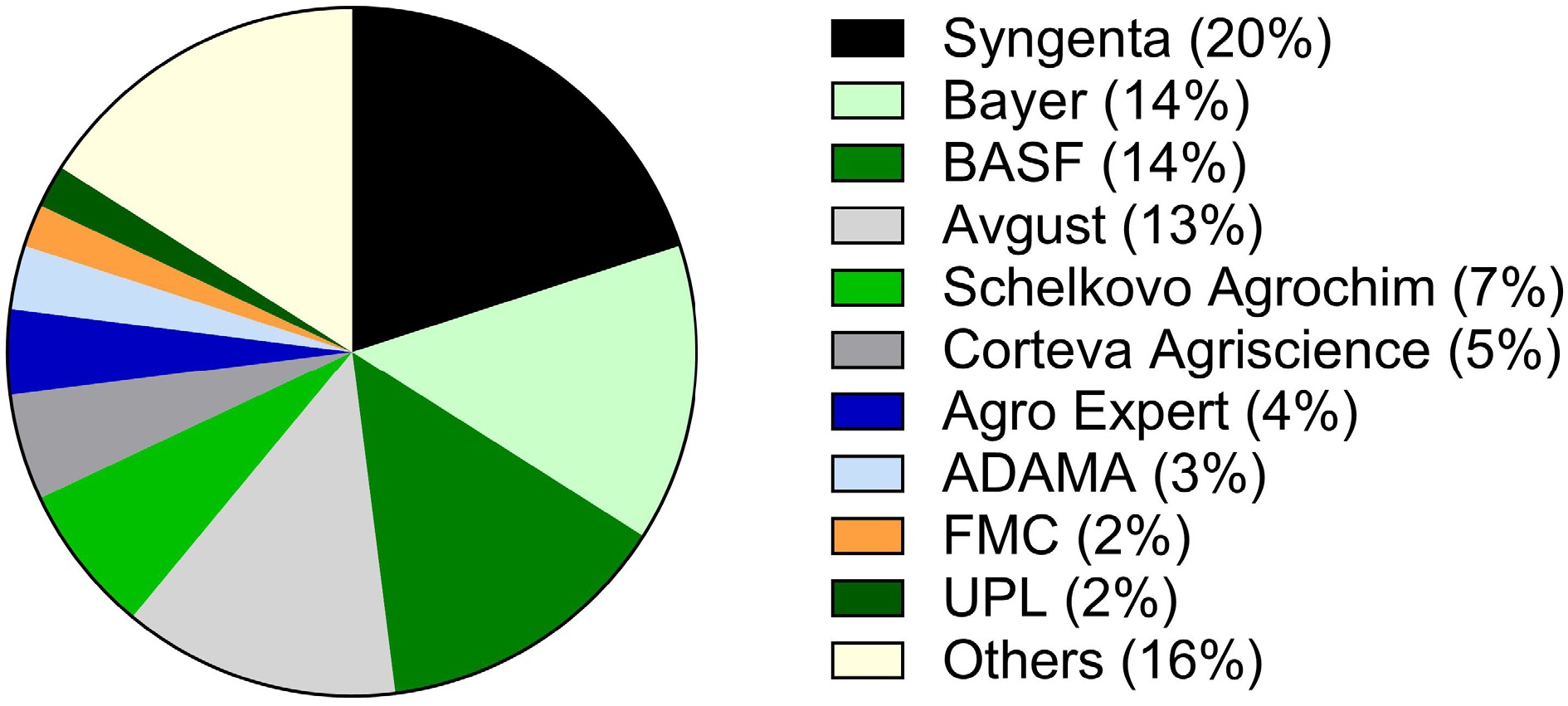

The most profound and lasting effect of the conflict on the global food market likely to be that more countries start to reconsider globalization. The economic sanctions imposed on Russia by Western countries are yet another reminder that economic activity is subordinate to geopolitics. Russia is likely to turn to the East to open up its markets. The global food market will be rearranged, potentially creating an imbalance between supply and demand. Food shortages in Africa will be exacerbated. Countries in the Middle East that rely heavily on grain imports will need to find new suppliers in the future. For this reason, the major players in the grain and fertilizer market will reconsider their global strategy (Fig. 4). This may further change the current geographical layout for production, transportation and destination of grain and fertilizers.

Figure 4.

Leading agrochemical players in Ukraine and Russia. Note: Splits are representative shares based on market research insights, not to be taken as exact values. Shares represent combined Ukraine and Russia market. Source: IHS Markit.

https://ihsmarkit.com/ It can be expected that food prices will remain high for a number of years. Judging by the geographical location of Donetsk and Luhansk, as they are located in the black soil area and belong to the main production area of crops (especially cereals), production, processing and transportation are bound to be adversely affected by the conflict. In terms of varieties, cereals as the basis of Ukrainian agriculture have been greatly affected, and it is expected that the degree of impact from high to low is wheat, barley, rye, corn, and the rise in grain prices will gradually affect the global market for Europe, or trigger the adjustment of feed formulations. It is also worthy to track the relationship between grain prices and meal prices in the coming years. In fact, general market concerns may also be a major factor pushing up the prices of related crops. The United Nations Global Food, Energy and Financial Crisis Response Team released a report saying that the world is facing the worst cost of living crisis since the 21st century due to factors such as the conflict in Ukraine. Greenspan also said, if the conflict continues, high prices of grains and fertilizers will continue into the next planting season, and there will be shortages of other basic foods such as rice, affecting billions of people around the world. Such concerns will surely be reflected in the market.

As for China, the conflict mainly affects the import of agricultural products, it directly affects the domestic supply of sunflower oil, corn and barley, of which sunflower seeds and corn are mainly affected by trade interruptions and short-term price increases brought about by sentiment, with little impact on long-term prices; Barley, on the other hand, may experience significant price increases as a result of the conflict. In addition, the conflict may affect the domestic pig breeding industry by affecting the cost of the industrial supply chain and accelerate the speed of capacity de-industrialization. Another effect on China is the traditional agriculture cooperation. In fact, as early as 25th May, 2012, the second meeting of the Agricultural Cooperation Subcommittee of the China-Ukraine Cooperation Committee was held in Kiev, Ukraine, and the Export-Import Bank of China, China Complete Engineering Co., Ltd., the Ministry of Finance of Ukraine, and the State Food and Grain Group of Ukraine signed the 'Framework Agreement on Cooperation in the Agricultural Field between China and Ukraine' with an agreement amounting to US

$\$ $ In short, the Russian-Ukrainian conflict has not only seriously affected the agricultural production and grain exports of Russia and Ukraine, but also seriously impacted the global grain market, mainly breaking the current grain supply and demand chain. In the short term, the price of grain and fertilizers has risen, and agricultural activities in some countries are partially influenced. Its long-term effects may challenge economic globalization, thereby changing the global pattern of food supply and demand. As a consequence, the agriculture and food markets may be overshadowed by geopolitics, aggravating the food crisis in more areas. The final impact of the conflict on global agriculture and food security still depends on when and how the conflict ends, whereas, this conflict has taught us an important lesson that food security is a top priority to all countries and agriculture must be vigorously developed to ensure self-sufficiency of food in order to effectively respond to any risks posed by unpredicted emergencies.

-

The author declares that there is no conflict of interest.

-

The opinions expressed in this article are those of the author and do not reflect the opinions of the journal.

- Copyright: 2022 by the author(s). Published by Maximum Academic Press on behalf of Hainan Yazhou Bay Seed Laboratory. This article is an open access article distributed under Creative Commons Attribution License (CC BY 4.0), visit https://creativecommons.org/licenses/by/4.0/.

Conflict of interest Disclaimer Rights and permissions (4) Table(1) - About this article

Cite this articleSun M. 2022. The impact of the Russia-Ukraine conflict on global grain market and food security: Short- and long-term effects. Seed Biology 1:3 doi: 10.48130/SeedBio-2022-0003

-

The impact of the Russia-Ukraine conflict on global grain market and food security: Short- and long-term effects

- Received: 24 July 2022

- Accepted: 24 July 2022

- Published online: 10 August 2022